Retirement is a significant milestone in one’s life, marking the transition from a career-focused existence to a more leisurely phase. While traditional pensions and savings have long been the primary sources of income during retirement, the changing economic landscape and increasing life expectancy have made it imperative for individuals to explore diverse income streams for financial security. It is crucial to look beyond the conventional sources and consider alternative options that can provide a stable and sustainable financial foundation for the post-work years.

Understanding Retirement Income Streams

Traditional Pensions Explained

Your retirement income streams may include traditional pensions, which offer a reliable source of income during retirement. These defined benefit plans typically provide a set amount of income based on years of service and earnings. While fewer employers offer traditional pension plans today, they remain a valuable asset for retirees, providing financial stability in addition to personal savings and other income sources.

The Role of Personal Savings and Retirement Accounts

The diversification of retirement income streams also involves personal savings and retirement accounts. Your contributions to employer-sponsored plans such as 401(k)s or individual retirement accounts (IRAs) play a crucial role in building a nest egg for retirement. These accounts offer tax advantages and potential investment growth, allowing you to supplement your pension income and meet your financial goals in retirement.

The Role of Personal Savings and Retirement Accounts

Government Benefits and Social Security

Another important aspect of retirement income diversification is government benefits, including Social Security. Social Security provides a foundation of income for many retirees and is designed to supplement other retirement income sources. Understanding how to maximize your Social Security benefits, as well as potential government assistance programs, can further enhance your financial security during retirement.

Role of Government Benefits and Social Security

Investment-Based Income Sources

Any retiree looking to diversify their income streams should consider investing in a variety of assets. This can help create a more stable and reliable source of income in retirement. For more information on how to diversify your sources of income in retirement, check out this informative guide.

Dividend-Paying Stocks

An attractive option for retirees seeking regular income is investing in dividend-paying stocks. These stocks provide shareholders with a portion of the company’s earnings as dividends, offering a steady stream of income. Dividend payments can provide a reliable source of income, especially when reinvested to purchase more shares or used to cover living expenses.

Bonds and Fixed-Income Securities

Income from bonds and fixed-income securities can be another important component of a well-diversified retirement income plan. These securities offer a predictable stream of income through regular interest payments. Bonds are generally considered less risky than stocks, making them a reliable source of income for retirees seeking stability in their investment portfolio.

Income from bonds and fixed-income securities is typically lower than potential returns from stocks or mutual funds. However, these investments provide a level of stability and security that can be valuable during retirement. It is important to consider your risk tolerance and investment objectives when incorporating bonds and fixed-income securities into your retirement income strategy.

Mutual Funds and Exchange-Traded Funds (ETFs)

Investment-based income sources such as mutual funds and exchange-traded funds (ETFs) offer diversification through a portfolio of multiple assets. These funds pool investors’ money to invest in a wide range of securities, providing exposure to different sectors and regions. Mutual funds and ETFs can offer a balanced approach to growth and income, providing retirees with a diversified source of cash flow.

Understanding the risks and potential returns of mutual funds and ETFs is crucial when incorporating them into your retirement income strategy. These investments can provide a significant income stream while allowing for passive management and diversification. It is important to research and select funds that align with your financial goals and risk tolerance.

Real Estate Investment Trusts (REITs)

On top of traditional stocks and bonds, retirees can also consider investing in Real Estate Investment Trusts (REITs) for additional income. REITs allow investors to access real estate markets without directly owning properties. Through REITs, retirees can earn income from rental properties, commercial real estate, and other real estate-related investments. Investing in REITs can provide retirees with a diversified income stream and exposure to the potential growth of the real estate market.

Stocks can be another valuable income source for retirees looking to diversify their investment portfolio. By investing in a mix of dividend-paying stocks, bonds, mutual funds, ETFs, and REITs, retirees can create a well-rounded income stream that offers both growth potential and stability in retirement. It is crucial to consult with a financial advisor to determine the most suitable investment options based on your financial goals and risk tolerance.

Passive Income Strategies in Retirement

For a secure retirement, it is crucial to diversify income streams beyond traditional pensions and savings. As highlighted in a recent article on Diversifying Your Investments for a Secure Retirement …, exploring various passive income strategies can provide financial security in retirement.

Rental Income from Real Estate

Any retirement income plan can benefit from incorporating rental income from real estate properties. Investing in rental properties can provide a steady stream of passive income, especially as property values appreciate over time. By carefully selecting properties in high-demand rental markets, retirees can enjoy a reliable source of income throughout their retirement years.

Royalties from Intellectual Property

Intellectual property, such as patents, trademarks, or copyrights, can also serve as a valuable source of passive income in retirement. By licensing out intellectual property rights, retirees can earn royalties from their creations without actively managing the day-to-day operations. This can be a lucrative opportunity for individuals with unique intellectual assets to generate additional income streams.

Passive income from royalties can be particularly advantageous for retirees seeking to supplement their retirement savings with ongoing revenue streams. By leveraging their intellectual property assets, retirees can enhance their overall financial stability in retirement.

Interest Income from Peer-to-Peer Lending

Income from peer-to-peer lending platforms can be a reliable source of passive income for retirees looking to diversify their investment portfolio. By lending out funds to borrowers through online platforms, retirees can earn attractive interest rates on their investments. With proper due diligence and risk management, peer-to-peer lending can offer retirees a consistent stream of passive income that can complement their retirement savings.

To achieve financial security in retirement, it is vital to explore and implement a mix of passive income strategies. By incorporating rental income from real estate, royalties from intellectual property, and interest income from peer-to-peer lending into a diversified income portfolio, retirees can create a robust financial foundation for their retirement years.

Utilizing Insurance Products for Retirement Income

Annuities as a Retirement Income Solution

Income streams in retirement are crucial for financial security, and one option to consider is annuities. An annuity is a financial product that provides regular payments over a specific period, often for the rest of your life. This can be a valuable tool for diversifying income streams beyond traditional pensions and savings. According to data, annuities offer a way to mitigate the risk of outliving your savings, providing a steady income source in retirement.

Life Insurance Policies with Cash Value Components

Value is another important aspect to consider when exploring insurance products for retirement income. Life insurance policies with cash value components can provide both protection and growth potential for your retirement portfolio. These policies offer the dual benefit of a death benefit for your beneficiaries and cash value that accumulates over time. This cash value can be accessed tax-free during retirement, offering an additional source of income to supplement your savings.

Policies with cash value components can provide flexibility in retirement planning, allowing you to access funds when needed while still preserving a portion for your beneficiaries. With the potential for growth and the added security of a death benefit, these policies can play a valuable role in diversifying your retirement income streams.

Longevity Insurance for Late-in-Life Security

Insurance can also be utilized as a tool for late-in-life security with longevity insurance. This type of product provides a guaranteed income stream starting at a specific age, typically later in life when other sources of income may be running low. Longevity insurance offers protection against the risk of outliving your savings and can provide peace of mind knowing that you have a secure income source in your later years.

Income from longevity insurance can supplement other retirement income streams, providing a reliable source of funds for imperatives like healthcare and daily living expenses. By incorporating longevity insurance into your retirement plan, you can create a more robust financial foundation for your later years, ensuring greater stability and security as you age.

Business Ownership and Part-Time Work

Running a Small Business in Retirement

Now, in retirement, many individuals are exploring the option of running a small business to supplement their income streams. According to a recent study, around 25% of retirees are entrepreneurs, leveraging their skills and experience to start businesses in various industries. By owning a business, retirees have the opportunity to create a steady income source while maintaining flexibility and control over their schedules.

Consulting and Freelance Opportunities

On the other hand, consulting and freelance opportunities can provide retirees with a way to capitalize on their expertise and industry knowledge. Many retirees find success in offering consulting services to businesses or working on freelance projects that align with their skills. These opportunities offer the flexibility to work on a project basis, allowing retirees to choose their workload and set their rates.

To fully take advantage of consulting and freelance opportunities, retirees should consider networking within their industry, setting up a professional online presence, and actively pursuing new clients. By showcasing their skills and experience, retirees can attract potential clients and secure lucrative projects.

The Gig Economy and Flexible Part-Time Work

Flexible part-time work in the gig economy has also become a popular choice for retirees looking to diversify their income streams. Research shows that around 30% of retirees are participating in the gig economy, taking on short-term contracts or freelancing assignments. This type of work offers retirees the flexibility to choose when and how much they want to work, providing a good balance between earning income and enjoying retirement.

This blend of entrepreneurship, consulting, and part-time work options provides retirees with a range of opportunities to diversify their income streams in retirement. By exploring these avenues, retirees can unlock new sources of income while staying active and engaged in their post-career lives.

Tax Considerations and Financial Planning

Despite the joy of retirement, financial planning remains a critical component of ensuring a secure retirement. Taxes play a significant role in retirement income planning, and understanding tax-efficient withdrawal strategies is imperative for maximizing your retirement income.

Tax-Efficient Withdrawal Strategies

Any comprehensive retirement income plan should consider the impact of taxes on your income streams. By strategically withdrawing funds from various accounts, such as taxable investment accounts, tax-deferred retirement accounts, and Roth accounts, you can minimize the tax burden on your retirement income. Consider consulting with a financial advisor to develop a tax-efficient withdrawal strategy tailored to your financial situation.

Managing Retirement Account Required Minimum Distributions (RMDs)

Required Minimum Distributions (RMDs) are mandatory withdrawals that you must take from your tax-deferred retirement accounts once you reach a certain age, typically starting at age 72. Failing to take RMDs can result in hefty penalties, so it’s crucial to plan for these distributions in your retirement income strategy.

Incorporating Health Care Costs and Insurance into Retirement Planning

With healthcare costs continuing to rise, incorporating health care expenses into your retirement plan is crucial for maintaining financial security in your golden years. Medicare provides imperative healthcare coverage for retirees aged 65 and older, but it doesn’t cover all expenses. Consider budgeting for supplemental insurance, long-term care insurance, and out-of-pocket medical costs to ensure you’re adequately prepared for healthcare expenses in retirement.

Summing up

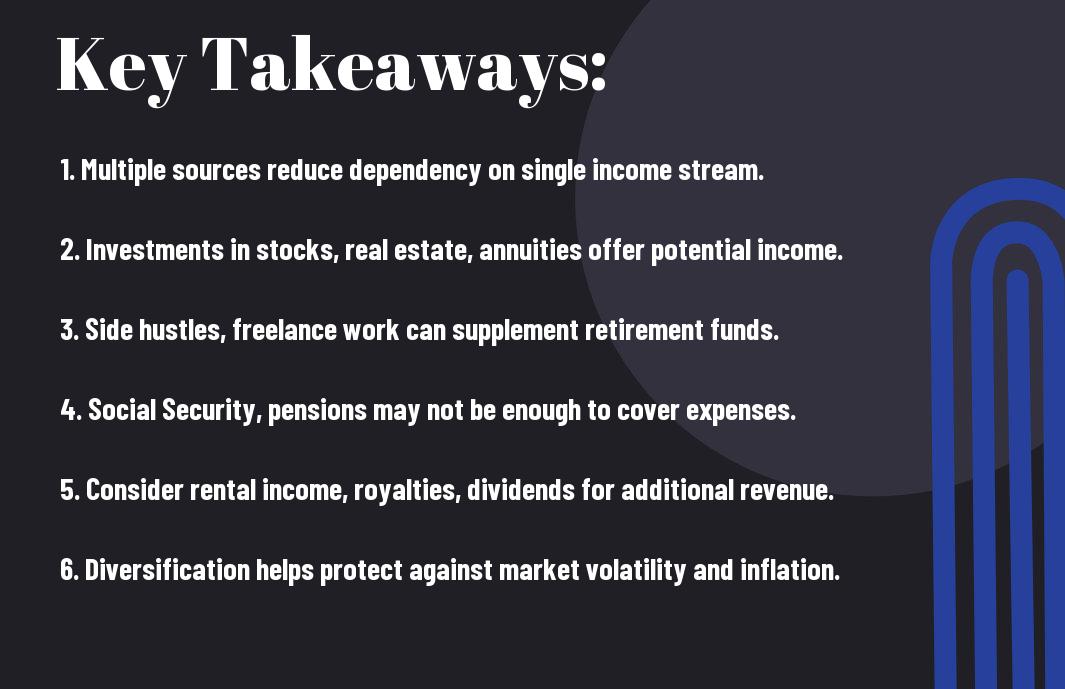

Ultimately, diversifying income streams in retirement is crucial for financial security and peace of mind. By exploring options beyond traditional pensions and savings, retirees can create a more robust and stable financial foundation for their golden years. Whether through investments, rental properties, part-time work, or other income-generating activities, having multiple streams of income can help offset any unexpected expenses and provide a more comfortable lifestyle in retirement. It is never too late to start diversifying your income streams and taking control of your financial future.

FAQ

Q: Why is it important to diversify income streams in retirement?

A: Diversifying income streams in retirement is crucial to ensure financial security and reduce the reliance on a single source of income, such as a pension or savings.

Q: What are some options beyond traditional pensions and savings for diversifying income in retirement?

A: Some options to consider for diversifying retirement income include rental properties, dividend-paying stocks, part-time work, freelance gigs, and starting a small business.

Q: How can diversifying income streams help in maintaining a comfortable lifestyle during retirement?

A: By diversifying income streams, individuals can supplement their pension and savings with additional sources of income, providing a cushion to cover unexpected expenses and maintaining a comfortable lifestyle in retirement.

Q: What are the risks associated with relying solely on traditional pensions and savings for retirement income?

A: Relying solely on traditional pensions and savings can be risky, as these sources of income may not be sufficient to cover all expenses in retirement, especially with increasing life expectancy and rising costs.

How can individuals start diversifying their income streams for retirement?

A: Individuals can start diversifying their income streams by assessing their skills and interests, exploring different investment opportunities, seeking financial advice, and gradually building additional sources of income over time to secure their financial future in retirement.