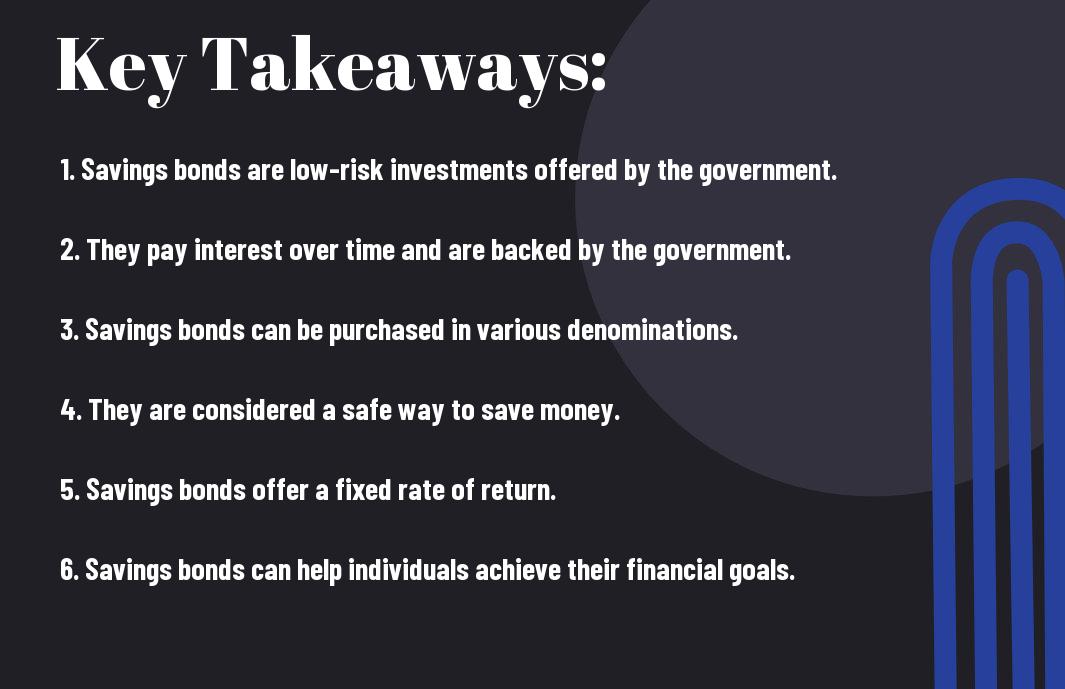

It’s imperative for individuals to explore various investment options to secure their financial future, and savings bonds offer a low-risk avenue worth considering. Savings bonds are issued by the government and provide a safe way to save money while earning a modest return over time. These bonds are considered one of the safest investment options available, making them an attractive choice for those looking to grow their savings without exposing themselves to significant risks.

Historical Context and Evolution of Savings Bonds

Development of Savings Bonds

For decades, savings bonds have served as a popular investment option for individuals looking for a low-risk way to save money. The concept of savings bonds dates back to the early 20th century when the U.S. government first introduced them as a way to finance military efforts during World War I. Since then, savings bonds have evolved to become a reliable and secure investment tool for individuals looking to grow their savings over time.

How Savings Bonds Have Changed Over Time

Evolution to meet the needs of savers has been a key factor in the changes seen in savings bonds over the years. Originally issued as paper bonds that required physical storage and safekeeping, savings bonds have adapted to the digital age with electronic bonds now being issued. This shift has made it easier for investors to purchase and manage their savings bonds online, streamlining the process and making it more convenient for savers to track their investments.

Bonds

Types of Savings Bonds

Any individual looking to invest in savings bonds has a variety of options to choose from. The most commonly issued savings bonds in the United States are Series EE Bonds and Series I Bonds. Both types of bonds offer a low-risk investment opportunity for individuals wanting to save for the future.

| Series EE Bonds | Series I Bonds |

|---|---|

| Low minimum investment of $25 | Indexed to inflation |

| Tax-deferred interest earnings | Fixed rate of return |

| Can be redeemed after one year | Some protection against inflation |

| Guaranteed to double in value in 20 years | Can be redeemed after one year |

| Interest accrues for up to 30 years | Interest accrues for up to 30 years |

Series EE Bonds

The Series EE Bonds are purchased at face value with a minimum investment of $25. These bonds earn interest for up to 30 years, and the interest earnings are tax-deferred. They can be redeemed after one year, but if held for 20 years, the bond will double in value, offering a guaranteed return on investment. These bonds provide a safe and secure way to save for the long term.

Series I Bonds

Redemption of Series I Bonds is available after one year, but they must be held for at least five years to avoid an early redemption penalty. These bonds are indexed to inflation and provide a fixed rate of return, offering some protection against the effects of rising prices. Series I Bonds are a popular choice for individuals looking to hedge against inflation while saving for the future.

Redemption: Series I Bonds can be redeemed after one year, but there is an early redemption penalty if they are cashed in before five years have passed. It is advisable to hold onto these bonds for a longer period to maximize returns and avoid penalties.

Maturity: The maturity period for Series I Bonds is 30 years, during which time they continue to accrue interest. Investors can choose to redeem the bonds at any point after the initial one-year holding period.

How to Purchase and Redeem Savings Bonds

Steps to Purchase Savings Bonds

After understanding the basics and benefits of savings bonds, the next step is to purchase them. The process of purchasing savings bonds is relatively straightforward. One common option is to buy electronic savings bonds through the TreasuryDirect website. You can also purchase paper savings bonds at select financial institutions. When buying savings bonds, you will need to provide personal information such as your Social Security Number and bank account details.

The Redemption Process

The redemption process for savings bonds varies depending on whether you have electronic or paper bonds. For electronic savings bonds, you can easily redeem them through your TreasuryDirect account. On the other hand, paper savings bonds need to be taken to a financial institution for redemption. Keep in mind that savings bonds have a minimum holding period before they can be redeemed without penalty, so it’s crucial to check the maturity date before attempting to cash them in.

For traditionalists who prefer paper savings bonds, the redemption process involves taking the physical bond to a financial institution, where it will be verified and redeemed. It’s important to note that if you choose to redeem your savings bond before it reaches its full maturity, you may incur a penalty equivalent to the most recent three months’ interest.

Understanding Interest Rates and Tax Benefits

All savings bonds come with fixed interest rates that are determined by the U.S. Department of the Treasury. These rates are typically set at the time of purchase and remain the same throughout the life of the bond. The determination of interest rates takes into account various factors, including current market conditions and the type of savings bond being issued.

Determination of Interest Rates

Benefits of savings bonds include the fact that they offer competitive interest rates compared to other low-risk investment options. The rates are typically higher than traditional savings accounts, making savings bonds an attractive choice for individuals looking to grow their savings over time without taking on excessive risk.

Tax Advantages of Savings Bonds

Rates of savings bonds can provide tax advantages for investors. The interest earned on savings bonds is exempt from state and local income taxes. In addition, if the funds from the bonds are used for qualified education expenses, the interest may also be exempt from federal income taxes. This can result in significant savings for investors over time.

Understanding the tax advantages of savings bonds can help individuals make informed decisions about where to invest their money. By taking advantage of these benefits, investors can maximize the growth of their savings while minimizing their tax liabilities.

Strategies for Incorporating Savings Bonds into Financial Planning

Savings Bonds as a Tool for Diversification

Your financial portfolio can greatly benefit from the inclusion of savings bonds as a tool for diversification. By investing in savings bonds, you are adding a low-risk option that can help balance out the volatility of other investments in your portfolio. With the potential to earn a fixed rate of return over a specific period, savings bonds provide a stable foundation for your financial future.

Long-Term vs. Short-Term Goals

To effectively incorporate savings bonds into your financial planning, it is important to consider your long-term and short-term financial goals. Bonds can be a great option for both types of goals. For long-term goals, such as retirement savings or education funds for children, investing in long-term savings bonds can provide a steady and reliable growth of your investment over time. For short-term goals, such as saving for a vacation or emergency fund, short-term savings bonds offer liquidity while still earning a competitive interest rate.

The Risks Associated with Savings Bonds

Inflationary Risks

Keep informed about the risks associated with savings bonds by regularly checking the official website of the U.S. Department of the Treasury. Visit About U.S. Savings Bonds for detailed information.

Liquidity and Accessibility

Associated with savings bonds is the risk of limited liquidity and accessibility. While savings bonds offer a low-risk investment option, they come with certain restrictions. Most savings bonds have a minimum holding period before they can be redeemed without penalty. It is crucial to carefully consider your financial goals and timelines before investing in savings bonds.

The limited liquidity of savings bonds can be a disadvantage for individuals who may need quick access to their funds in case of emergencies or unforeseen expenses. It is important to assess your financial situation and determine if the restrictions associated with savings bonds align with your needs.

Future Trends and Innovations in Savings Bonds

Technological Advances and Savings Bonds

Despite being considered a traditional investment vehicle, savings bonds are not immune to technological advancements. Digital platforms have made it easier for individuals to purchase and manage their savings bonds online, eliminating the need for physical paperwork and streamlining the process.

Legislative and Economic Factors

Bonds have historically been influenced by legislative and economic factors, and this trend is expected to continue in the future. Changes in interest rates, inflation rates, and government policies can impact the performance of savings bonds, making it necessary for investors to stay informed and adapt their investment strategies accordingly.

- Recognizing the potential impact of these factors, investors should diversify their portfolios to mitigate risks and maximize returns.

The intersection of legislation and economics plays a crucial role in shaping the landscape of savings bonds. Government regulations, tax laws, and economic conditions can all affect the attractiveness of savings bonds as an investment option.

- Recognizing the immense potential of savings bonds, governments around the world are continuously exploring ways to make them more appealing to investors while ensuring financial stability.

Innovation within the savings bond sector is also on the rise, with the introduction of new bond products, such as inflation-protected bonds and digital savings bonds, catering to the evolving needs of investors. These innovations aim to provide investors with more flexibility, higher returns, and better protection against market fluctuations.

To wrap up

From above, savings bonds provide a low-risk investment opportunity for individuals looking to save money over a period of time. These bonds are issued by the government and offer a fixed interest rate that is guaranteed to be paid to the bondholder upon maturity. With various types of savings bonds available, including EE savings bonds and I savings bonds, investors have the flexibility to choose the option that best suits their financial goals.

Overall, savings bonds provide a secure and reliable way to save money, with the added benefit of earning a return on your investment. Whether you are saving for a specific goal or simply looking to grow your wealth over time, savings bonds can be a valuable addition to your investment portfolio. Consider exploring the world of savings bonds to see how they can help you achieve your financial objectives.

FAQ

Q: What are savings bonds?

A: Savings bonds are a type of government-issued investment product that offer a low-risk way for individuals to save money over time.

Q: How do savings bonds work?

A: When you purchase a savings bond, you are necessaryly lending money to the government. In return, the government pays you interest on the bond over a set period of time.

Q: What are the benefits of investing in savings bonds?

A: Savings bonds are considered to be a safe investment option as they are backed by the government. They also offer a fixed rate of return, which can provide a stable source of income.

Q: Are savings bonds a good option for individuals looking to save for the long term?

A: Yes, savings bonds can be a good choice for long-term savings goals, as they typically have a maturity date of several years, allowing your investment to grow over time.

Q: How can I purchase savings bonds?

A: Savings bonds can be purchased directly from the U.S. Department of the Treasury through their website, or through financial institutions such as banks and credit unions.