Just as planning for retirement involves saving for the future, it also requires careful consideration of healthcare expenses. Health Savings Accounts (HSAs) and Medicare are two valuable tools that can help individuals navigate the complexities of healthcare costs during retirement. Understanding how to utilize HSAs effectively and make informed decisions when transitioning to Medicare can lead to significant savings and peace of mind in your retirement years.

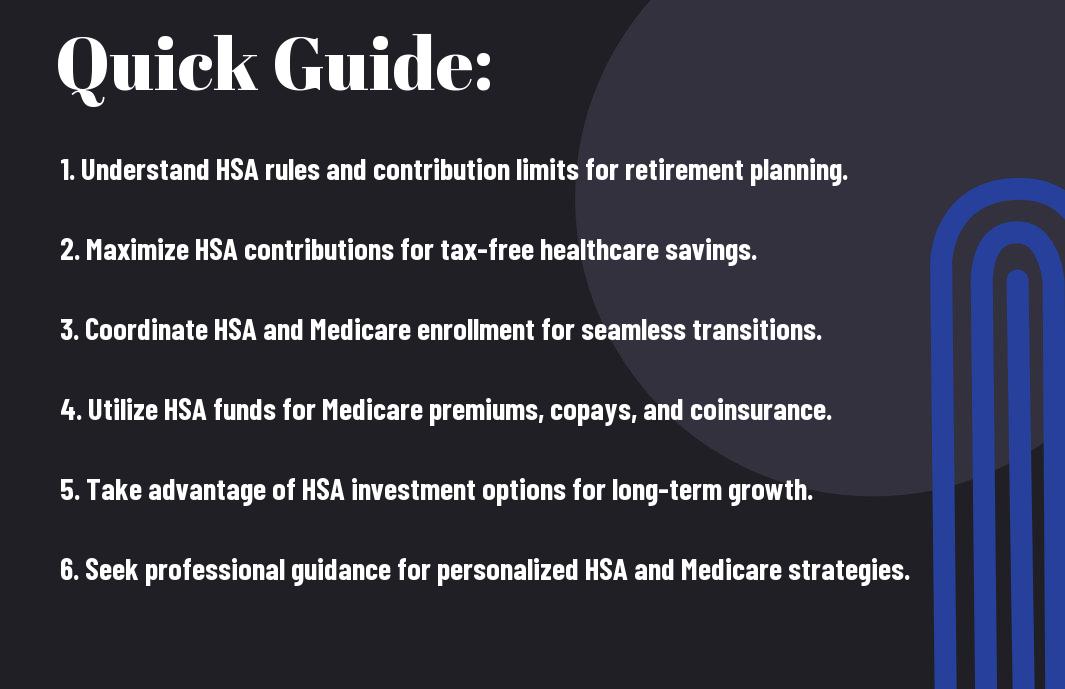

Key Takeaways:

- Health Savings Accounts (HSAs) are a valuable tool for saving for healthcare costs in retirement. Utilize pre-tax contributions to grow savings over time for medical expenses.

- Understand the eligibility requirements and contributions limits for HSAs. Make sure to maximize contributions each year to build a solid healthcare savings fund.

- When approaching Medicare eligibility, coordinate your HSA contributions to avoid penalties. Know the rules for HSA contributions and Medicare enrollment to optimize your healthcare savings strategy.

- Consider Supplemental Insurance options to complement Medicare coverage. Medigap or Medicare Advantage plans can help fill gaps in coverage and reduce out-of-pocket expenses.

- Consult with a financial advisor or healthcare specialist to create a comprehensive plan for retirement healthcare savings. Get personalized advice on how to best utilize HSAs, Medicare, and other resources for optimal healthcare savings.

Understanding Health Savings Accounts (HSAs)

Some 5 ways HSAs can help with your retirement include tax savings, long-term investment growth potential, and flexibility in healthcare spending. As healthcare costs continue to rise, HSAs have become a valuable tool for individuals to save for medical expenses both now and in retirement. By contributing to an HSA, you can enjoy tax deductions on your contributions, tax-free growth on your investments, and tax-free withdrawals for qualified medical expenses.

What is an HSA?

An HSA is a tax-advantaged savings account that allows individuals with a high-deductible health plan to save money for medical expenses. Contributions to an HSA are tax-deductible, and funds can be used tax-free for qualified medical expenses, including deductibles, copayments, and prescriptions. HSAs offer a triple tax advantage, making them a powerful tool for saving for healthcare costs in retirement.

HSA Investment Strategies

Even with the tax advantages of an HSA, many account holders may not be aware of the potential for long-term growth through strategic investment. By utilizing HSA investment options, such as mutual funds or ETFs, individuals can potentially grow their savings over time, maximizing the benefits of their account. Investment in a diversified portfolio can help offset future medical expenses in retirement and provide additional financial security.

Investment in an HSA should align with your risk tolerance and long-term financial goals. Consider consulting with a financial advisor to develop an investment strategy that suits your needs and maximizes the growth potential of your HSA funds.

Making the Most of Your HSA

Despite the myriad of options available for healthcare savings, Health Savings Accounts (HSAs) stand out as a valuable tool for individuals looking to maximize their retirement healthcare funds. One key aspect of utilizing an HSA effectively is understanding how to strategically utilize the funds within the account to cover medical expenses both now and in the future.

The Smart Use of HSA Funds

One smart way to make the most of your HSA funds is to prioritize using them for qualified medical expenses, such as doctor visits, prescriptions, and other healthcare services. By using your HSA funds for these expenses, you can benefit from the tax advantages of the account while ensuring that your healthcare costs are effectively covered. Additionally, considering future healthcare needs and saving a portion of your HSA funds for retirement can help you build a robust healthcare savings plan for the long term.

HSA Management at Retirement

Making strategic decisions about how to manage your HSA funds at retirement is crucial for optimizing your healthcare savings. One common strategy is to continue using your HSA funds for qualified medical expenses in retirement to supplement other healthcare coverage, such as Medicare. By doing so, you can stretch your healthcare dollars further and potentially reduce out-of-pocket costs during retirement.

Prospective Strategies for Managing HSA Funds at Retirement

| Continue to use HSA funds for qualified medical expenses in retirement | Supplement other healthcare coverage, such as Medicare, with HSA funds |

The Basics of Medicare

All individuals nearing retirement age should have a solid understanding of Medicare. It is a federal health insurance program primarily for people aged 65 and older, as well as certain younger individuals with disabilities. To better comprehend Medicare, it’s important to distinguish between its different parts – Part A, Part B, Part C, and Part D. If you are interested in utilizing your Health Savings Account (HSA) effectively as a retirement savings tool, check out this guide on how to use your HSA as a retirement savings tool.

Understanding the Different Parts of Medicare

While Part A covers hospital care, skilled nursing facilities, hospice, and limited home health services, Part B relates to medical services like doctor visits, outpatient care, and preventive services. Part C, also known as Medicare Advantage, combines Part A and Part B coverage and is offered through private insurance companies. Part D focuses on prescription drug coverage. Understanding these different parts can help you make informed decisions about your healthcare coverage during retirement.

Enrollment Periods and Late Enrollment Penalties

Part of navigating Medicare involves being strategic about enrollment periods to avoid late enrollment penalties. For most people, the Initial Enrollment Period for Medicare starts three months before turning 65 and extends for seven months. Failing to enroll during this period may result in higher premiums and delayed coverage. It’s crucial to weigh your options and enroll in Medicare at the right time to avoid unnecessary financial penalties down the road. Different parts of Medicare also have specific enrollment periods and rules, so it’s important to stay informed and plan accordingly for your healthcare needs in retirement.

Strategies for Integrating Medicare and HSAs

Factors to Consider When Combining HSA and Medicare

Unlike traditional employer-sponsored health plans, Medicare and Health Savings Accounts (HSAs) have specific rules and regulations that must be understood when integrating the two for optimal healthcare savings. When combining Medicare with an HSA, it is important to consider factors such as eligibility requirements, contribution limits, and tax implications.

It is crucial to be aware that individuals cannot contribute to an HSA once they are enrolled in Medicare, as this violates IRS rules. However, if you were previously enrolled in an HSA-compatible high-deductible health plan before enrolling in Medicare, you can still use the funds in your HSA for qualified medical expenses. Thus, planning ahead for this transition is vital to avoid any penalties or tax complications.

- Understanding the timing of enrolling in Medicare and how it impacts HSA contributions

- Being aware of the rules around using HSA funds for medical expenses after enrolling in Medicare

- Seeking guidance from a financial advisor or healthcare consultant specialized in retirement planning

Though navigating the complexities of integrating Medicare and HSAs may seem daunting, being well-informed and proactive in your approach can lead to significant healthcare savings in retirement.

Coordinating Medicare with Other Health Coverage

Any individual approaching retirement age should be mindful of how Medicare interacts with other health coverage options, such as employer-sponsored plans, COBRA, or private insurance. Coordinating these different forms of coverage requires careful consideration and planning to ensure seamless transitions and avoid any gaps in healthcare coverage.

Medicare plays a critical role in providing health benefits for individuals aged 65 and older in the United States. It is important to enroll in Medicare on time to avoid any late enrollment penalties and disruptions in coverage.

With the rising costs of healthcare in retirement, understanding how to coordinate Medicare with other health coverage options is vital for maintaining comprehensive healthcare benefits without breaking the bank.

Maximizing Healthcare Savings in Retirement

Tips for Reducing Healthcare Costs with Medicare

Keep your healthcare costs in check during retirement by taking advantage of the cost-saving benefits offered by Medicare. Some necessary tips include choosing the right Medicare plan that aligns with your healthcare needs and budget, exploring options for supplemental insurance to cover gaps in coverage, and staying informed about preventive services and screenings covered by Medicare to detect and address health issues early.

- Choose the right Medicare plan for your needs

- Explore supplemental insurance options

- Stay informed about covered preventive services

Perceiving the complexities of Medicare can be overwhelming, but with the right knowledge and proactive approach, you can effectively reduce your healthcare costs and ensure comprehensive coverage during retirement.

Utilizing HSA and Medicare in Tandem

Unlock additional healthcare savings potential by leveraging Health Savings Accounts (HSAs) alongside Medicare coverage. Options such as funding your HSA with pre-tax dollars, using HSA funds to cover eligible medical expenses not covered by Medicare, and maximizing your HSA contributions to build a healthcare nest egg can help you achieve significant savings in retirement.

With careful planning and strategic utilization of both HSAs and Medicare, you can optimize your healthcare savings and ensure financial stability in retirement. Consult with healthcare and financial professionals to explore personalized strategies that align with your specific needs and goals.

Case Study: HSAs and Medicare in Action

Not only can Health Savings Accounts (HSAs) provide significant savings on healthcare expenses, but they also play a crucial role in preparing for retirement healthcare costs. Let’s look at a case study to understand how HSAs and Medicare can work together to maximize savings and ensure comprehensive healthcare coverage.

In this case, a 55-year-old individual has been contributing to an HSA for the past ten years and has built up a considerable savings balance. By taking advantage of the tax benefits associated with HSAs, they have accumulated funds that can be used for qualified medical expenses both now and in retirement.

As the individual approaches age 65, they begin to transition from their employer-sponsored health insurance to Medicare. While Medicare provides comprehensive coverage for many healthcare services, it doesn’t cover everything. This is where the HSA comes into play.

The individual continues to use their HSA funds to cover out-of-pocket costs associated with Medicare, such as deductibles, copayments, and services not covered by Medicare. By doing so, they can minimize their overall healthcare expenses and ensure they have adequate funds set aside for any future healthcare needs.

Furthermore, the HSA continues to grow tax-free, allowing the individual to build a nest egg specifically earmarked for healthcare costs in retirement. This provides peace of mind knowing that they have a dedicated source of funds to cover future medical expenses.

By strategically utilizing both HSAs and Medicare, this individual has been able to maximize their healthcare savings, minimize out-of-pocket expenses, and ensure they have comprehensive coverage well into retirement. This case study highlights the value of incorporating HSAs into your overall healthcare savings strategy and understanding how they complement Medicare to provide a solid foundation for your healthcare needs.

Common Mistakes to Avoid

After reading about the 5 smart ways to manage healthcare costs during retirement, it’s crucial to avoid common mistakes that can derail your savings efforts. Missteps with HSA Contributions and Distributions can have significant financial consequences. Some may contribute too much to their HSA, unaware of the contribution limits set by the IRS. This can result in penalties and added tax burdens. On the other hand, some may not utilize their HSA funds wisely, missing out on the tax advantages offered by these accounts. It’s crucial to understand the rules and regulations governing HSA contributions and distributions to maximize your savings potential in retirement.

Missteps with HSA Contributions and Distributions

Some may contribute too much to their HSA, unaware of the contribution limits set by the IRS. This can result in penalties and added tax burdens. On the other hand, some may not utilize their HSA funds wisely, missing out on the tax advantages offered by these accounts. It’s crucial to understand the rules and regulations governing HSA contributions and distributions to maximize your savings potential in retirement.

Pitfalls in Medicare Enrollment and Plan Choice

Distributions from HSAs have some limitations, and understanding these rules is imperative to avoid penalties or tax implications. In the matter of Medicare enrollment and plan choice, many retirees may make hasty decisions that don’t align with their healthcare needs. Plan. It’s crucial to carefully evaluate your options and choose the Medicare plan that best fits your health requirements and budget. Making informed choices can lead to significant cost savings in the long run.

FAQs on HSAs and Medicare

Addressing Frequent Concerns

To ensure you are making the most informed decisions regarding your healthcare savings, it’s important to address some common concerns about HSAs and Medicare. One frequent question is, “Can I have both an HSA and Medicare?” The answer is yes, you can have both, but there are eligibility requirements to consider. Individuals enrolled in Medicare are not able to contribute to an HSA, but if you delay enrolling in Medicare and continue to have a high deductible health plan, you can still contribute to your HSA.

Clarifying Complex Scenarios

Any individual approaching retirement age may find themselves in unique situations with regards to HSAs and Medicare. Some scenarios to consider include the impact of HSA contributions on Medicare premiums and the rules around using HSA funds for Medicare premiums. For example, contributions to an HSA are tax-deductible and can reduce your taxable income, potentially lowering your Medicare premiums. Additionally, HSA funds can be used tax-free for qualified medical expenses, including Medicare premiums in certain circumstances.

Plus, it’s important to understand that while HSAs offer tax advantages and flexibility for saving for healthcare expenses, the rules and regulations surrounding Medicare can be intricate. Consulting with a financial advisor or healthcare specialist can provide further clarification on how to optimize your healthcare savings through the use of HSAs and Medicare.

Summing up

To wrap up, Health Savings Accounts (HSAs) can be a valuable tool for saving money for healthcare expenses both now and in retirement. By taking advantage of the tax benefits and flexibility of HSAs, individuals can build up a significant nest egg to cover medical costs in their later years. It’s important to carefully consider contributions, investment options, and eligible expenses to make the most of your HSA and maximize your savings potential.

In the context of Medicare, understanding the different parts and what each covers is crucial for optimizing your retirement healthcare savings. Making informed decisions about when to enroll, which plans to choose, and how to supplement your coverage with additional insurance can help you minimize out-of-pocket expenses and ensure comprehensive care. By combining the benefits of HSAs with the coverage options provided by Medicare, you can create a solid financial strategy for your healthcare needs as you transition into retirement.